Deposit insurance is one of the biggest pros of having an account at an FDIC (Federal Deposit Insurance Corporation)-insured bank. An FDIC-insured bank protects your money in the event of an unlikely bank failure. Keep reading to learn the benefits of being covered by an FDIC-insured bank.

What is FDIC Insurance?

FDIC insurance is a significant benefit of putting your money in a bank that is FDIC insured. “The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category.” Simply banking with an FDIC-insured bank takes away having to purchase deposit insurance, as you are automatically covered. FDIC insurance maximizes your protection.

What Does FDIC Insurance Typically Cover?

Just because a banking institution offers FDIC insurance, that does not necessarily mean all accounts, products, and investments are covered.

FDIC insurance often covers:

-

Checking Accounts

-

Savings Accounts

-

Money Market Accounts

-

Certificates of Deposits

-

Cashier’s Checks or Money Orders

-

Negotiable Order of Withdrawal Accounts

The FDIC does not cover:

-

Stock Investments

-

Bond Investments

-

Mutual Funds

-

Annuities

-

Safe Deposit Boxes

-

Life Insurance Policies

-

U.S. Treasury Bills, Bonds, or Notes

Remember, if your bank is an FDIC-insured institution, coverage is automatic to you, there is no need to apply for FDIC insurance.

Are You Covered?

The amount of FDIC insurance coverage you may be entitled to depends on the FDIC ownership category. So, to help you best understand what accounts are covered and the coverage you are entitled to, please check out the example below.

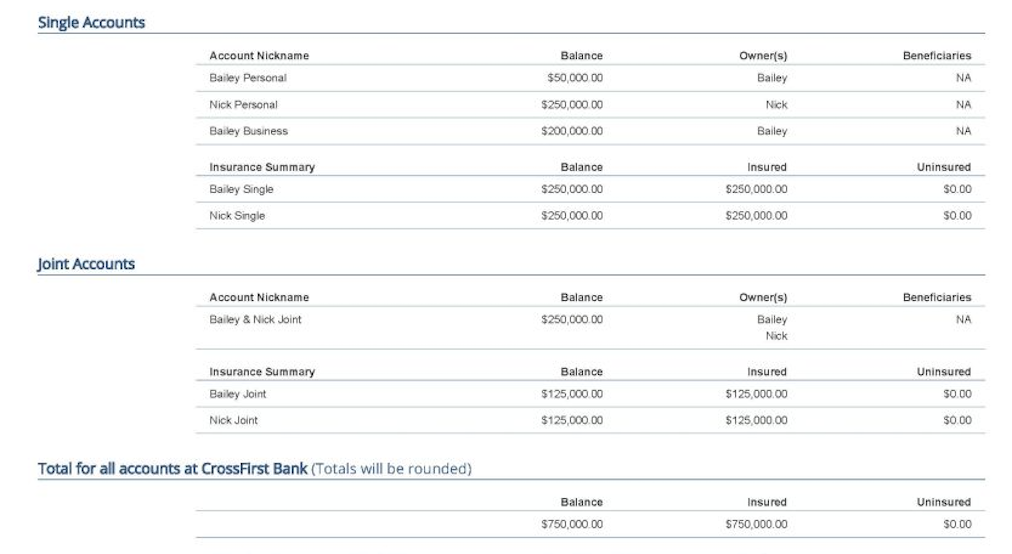

Bailey and Nick are married. Their bank is FDIC insured. Between the two of them, Bailey and Nick both have their own separate single ownership account as well as share a joint account they are equal parts to. On top of their single and joint accounts, Bailey is a small business owner.

Single Ownership Account: Applies to a deposit account owned by one person without named beneficiaries, including checking, savings, and money market deposit accounts. The coverage limit of all single accounts owned by the same person at the same bank are added together and insured up to $250,000.

Joint Account: A joint account is owned by two or more people, without named beneficiaries. The biggest takeaway of a joint account in comparison to a single ownership account is they are in two different categories. To qualify for coverage with a joint account the owners must be living, have equal rights to withdrawal, and sign the deposit account signature card. Joint accounts are covered for up to $250,000 per owner or a total of $500,000 between the same two owners.

Business Account: FDIC insurance treats business accounts the same as personal accounts. Business accounts for corporations, partnerships and unincorporated associations get the full $250,000 in FDIC coverage, separate from any owner or member. The coverage limit of a business account is added together and insured up to $250,000, separately from the personal accounts of the owners or members. However, a sole proprietorship falls under a single ownership account so the owner needs to stay below the $250,000 threshold between both their sole proprietorship and their personal single ownership accounts.

This is what our example looks like when we plug it into the Electronic Deposit Insurance Estimator:

In conclusion, you can see all of Bailey and Nick’s accounts are insured by FDIC so long as they do not go over $250,000 in either the single or joint account categories. If you want to check out detail for your accounts, utilize the tools below to check if your bank is insured, which of your accounts are covered, and how much coverage you have.

Is Your Bank Institution Insured? – Not all banks are FDIC insured. Check if yours is on the list (CrossFirst is)!

Are Your Deposit Accounts Insured? – Not all accounts, products, and investments are covered by FDIC insurance. Learn more about the types of accounts that are covered.

Use EDIE or Electronic Deposit Insurance Estimator to determine if you, your family, and your business is covered.

Frequently Asked Questions About Deposit Insurance

If you are interested in FDIC deposit insurance coverage, remember that it’s automatic as long as you are placing your funds in a deposit product at the bank and you do not go over the coverage limits by ownership category. If you are unsure about your specific situation, we are happy to help.